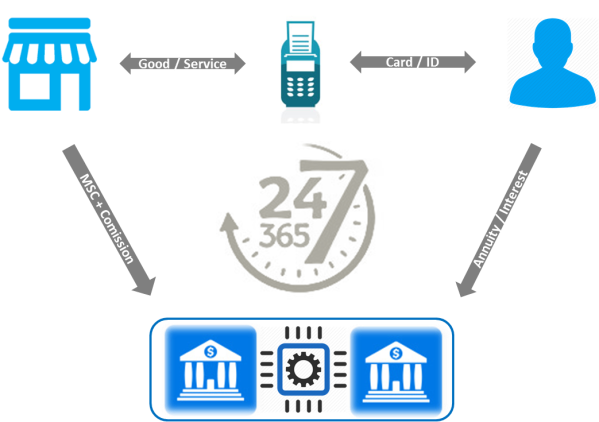

The traditional payment system is based on a model in which four parties are involved: the issuer, the acquirer, the cardholder and the merchant. In this system, two banks are always involved and the rendering of payment services is guaranteed from the issuer to the cardholder and from the acquirer to the merchant.

The bank card payment scheme is agreed between the issuing bank and acquiring bank and a fifth entity (VISA or Master Card) which defines the procedures and rules of authentication, authorisation and settlement of a financial transaction and facilitates use of the electronic payment inside the country where the transaction was made and abroad.

The issuing bank agrees the payment terms of the purchase of goods and services with the cardholder. The acquiring bank agrees the conditions of sale of goods and services by card with the merchant.

In the global market associated to the four-part model, niches develop in the marketplace between any two of its players: the market between merchants and acquirers; the market between acquirers and issuers; the market between consumers and issuers; and the market between merchants and consumers.

Let us follow the money funding flow from the merchant: the bank supporting the merchant (acquirer) aims to garner the maximum of merchants to its network of acceptance in order to provide them a safe service of receipt of their sales of goods and/or services in exchange for a monthly fee to the support bank and a service fee to the merchant applied per transaction performed.

The acquirer shares part of the service fee charged to the merchant with the issuing bank – the interchange fee. The more merchants that accept electronic payments and the more customers who are holders of payment cards, the greater the invoicing of services provided by the support banks to these. The acquirer bank guarantees the act of receiving and the issuing bank guarantees the payment.

The consumer wants to make payments at any time and in any place without having to go to the bank or to withdraw money or to give payment instructions. The issuing bank provides its client with a payment card so that the customer can give it instructions by electronic payment. By this facility, the customer pays the commission regarding the annuity fee of the card. In the case of a credit card, the customer may have to pay additional interest, if the payment of the capital used is made, after the period up to 50 days of free credit has passed. There may still accrue other fees for services (e.g. urgent card reissuance with detour to a specific address).

Finally, the merchant, on receiving the digital indication of payment, provides the goods or services rendered to the cardholder, his customer, thereby finalising the commercial economic transaction (whether physical or online).

In certain cases, the issuing bank and the acquiring bank may be the same entity. In this situation we have a model in which only three parties are involved. See the examples of AMEX – American Express, where it is this entity that contracts the terms of payment and receipt with the cardholder and the merchant, respectively.

Any of the models represent an Ecosystem, in real time, constantly working to provide the cardholder and the merchant with a nice and easy user experience. All the stakeholders favour cost, risk, security, privacy and speed.

It can be added that the payments industry, like others, is based on the economic concept “two-sided platform.” To explain this concept, observe the credit card market, made up of cardholders and merchants. In this example, the greater the value each participant has on the one side of the economic platform, the greater the number of participants on the other side of the platform. The more cardholders, the greater number of POS and vice-versa.

A Payments Ecosystem is, then, the system where payments are made (pay before, pay now, pay later), which includes the form (physical, electronic, digital), the means (cash, check, card, transfer, direct debit) and the channels used (shop / kiosk / Agent, Call Center, ATM, POS, Web, Mobile) with the ability to influence the economic players involved in the economy.

One can note the evolution of banking channels of renowned economic players, such as CitiGroup, Santander, Unicredit and HSBC (Branch concept – 1970s), First Direct (Call-Center concept – 1980s), Smile (Internet concept -1990s), and Moven (Mobile concept – 2000 and following).

How has the payment ecosystem evolved since the 1950s?

[…] Payments Ecosystem 1/5 11/02/2016 […]

LikeLike

[…] Payments Ecosystem 1/5 – DESAFIOS DA GESTÃO ESTRATÉGICA 11/09/2016 at 16:15 Reply […]

LikeLike